Common TFSA mistakes

Investment insight

Tax-free savings accounts (TFSAs) have become popular savings vehicles. While millions of Canadians have opened a TFSA, many are still making mistakes or missing opportunities that are costing them money.

Things you might not know about TFSAs but should

A TFSA is a flexible, general-purpose savings vehicle that allows you to make contributions each year and to withdraw funds at any time in the future. A TFSA provides a powerful incentive to save by allowing the investment growth to accumulate each year and be withdrawn tax free. However, unlike a registered retirement savings plan (RRSP), you can’t claim a tax deduction for contributions made to your TFSA and withdrawals are added back to your contribution room for the following year.

Withdrawal or transfer?

You can transfer from one TFSA to another provided the funds go directly to the new plan without having been paid to you first. If the funds are paid to you first, it’ll be considered a withdrawal and your TFSA room for the withdrawal amount won’t be reinstated until the next calendar year. Recontributing to a TFSA in the same year as the withdrawal may result in an overcontribution and you could be subject to a penalty tax.

The Income Tax Act (Canada) imposes a penalty of 1% per month on the highest excess contribution amount at any time during the month. The excess amount can be withdrawn to eliminate the penalty tax for subsequent months.

Spouse as beneficiary or successor holder?

If your spouse1 is named as the beneficiary of the TFSA, an amount up to the value of the TFSA at the time of death can be contributed to your spouse’s TFSA without affecting the TFSA contribution room. But this can only happen if the contribution is made before the end of the year following the year of death and is designated as an exempt contribution. Any income earned between the date of death and the contribution will be taxable to your spouse.

It’s often recommended that, where permitted, the holder name a spouse as successor holder instead of as beneficiary.2 On the holder’s death, the spouse will automatically become the new holder of the TFSA. The TFSA continues to exist, and both its value at the date of death and any income earned after that date continue to be sheltered from tax under the new successor holder. In addition, naming a spouse as successor holder avoids the administration and filing requirements necessary to preserve the tax-free status of the TFSA funds when a spouse is named as beneficiary.

U.S. citizens with a TFSA

U.S. citizens, even those living in Canada, or other U.S. persons (e.g., green card holders) are required to report their worldwide income to the Internal Revenue Service (IRS) each year, including any income earned in their TFSA, as there’s no treaty relief for TFSAs. Whether U.S. taxes will ultimately have to be paid will depend on the particular facts and whether sufficient foreign tax credits are available. Such individuals should speak to a cross-border tax specialist before investing in a TFSA.

Trading too actively in a TFSA

You can trade various securities in your TFSA, such as stocks, bonds, or exchange traded funds (ETFs). Generally, the gains from securities traded in a TFSA are tax free; however, there are circumstances where gains in your TFSA could be fully taxable as business income. To make this determination there are a number of factors that the Canada Revenue Agency (CRA) would consider:

- nature of the trading activity

- trading frequency and volume

- how long the securities are held

- intention to acquire and sell the securities at a profit

- time spent researching and trading

If you actively trade in your TFSA, speak to your tax advisor about whether this tax treatment could apply to you.

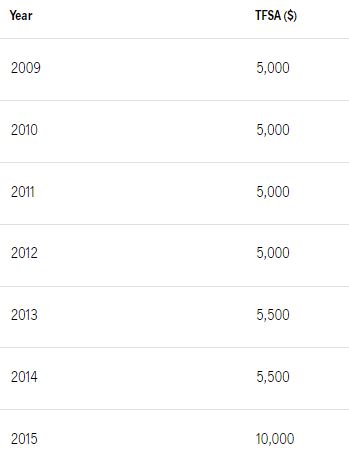

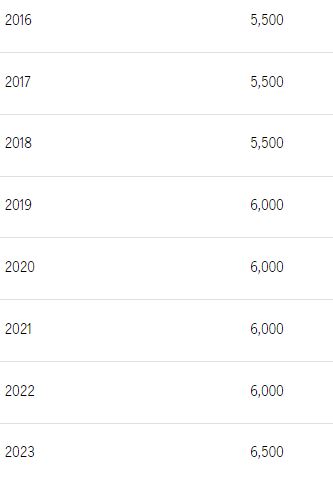

TFSA contribution limit

Since TFSAs were made available in 2009, individuals have been able to make contributions up to the legislative dollar maximum per year. If you don’t contribute the full amount, any unused amount will carry forward to the next year. Unused contribution room can be carried forward indefinitely.

Annual contribution limits for TFSAs

Summary

TFSAs are powerful savings vehicles whose significance will only grow over time. However, to fully maximize the benefits and avoid the pitfalls, it’s important to speak to your advisor to understand how they work.

![]()