Individual pension plans and the family business

With changes to pension limits and the ability to include an individual pension plan (IPP) in a succession plan, IPPs have become the registered retirement savings plan (RRSP) alternative for many business owners. Normally, on the death of the surviving spouse,¹ registered assets create a tax liability in the estate. An IPP for a family business can be an effective way of transferring registered assets to the second generation on a tax-deferred basis.

What’s an individual pension plan?

An IPP is a defined benefit pension plan. If you’re a business owner, an IPP offers both maximum tax relief and a maximum retirement pension.

The result?

You won’t have to rely solely on your RRSP’s performance to provide a long and happy retirement. That’s because IPPs also offer guaranteed lifetime income and any surplus in the plan may be payable to you.

Why are IPPs so popular?

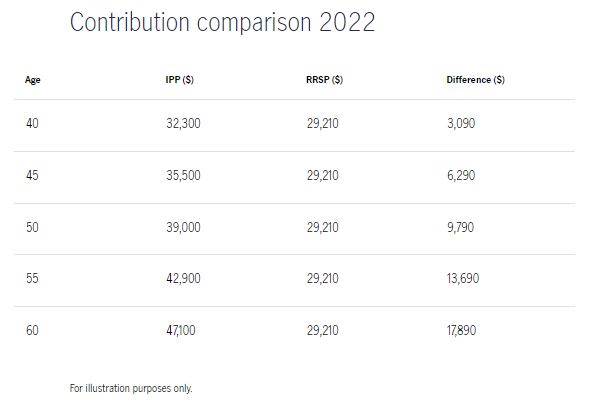

The maximum pension limit for 2022 is $3,420 per year of service. This limit is subject to increases based on the average industrial wage.

At age 50, the annual maximum contribution is $9,790 higher than the maximum contribution to an RRSP. As you get closer to retirement, the cost to provide the benefit increases. You can also include service back to 1991. This is optional, but if you decide to include extra years, it’ll significantly increase the amount that can be deposited into the plan.

Opportunities

A family business

Normally on the death of the surviving spouse, registered assets create a tax liability in the estate. An IPP is an ideal way to keep the assets in a tax-deferred vehicle when involving a family business.

If the business is continuing after the parent retires, the family member (usually a son or daughter) who takes over the business can be added as a member of the existing plan. By leaving the plan intact, any assets not used to provide benefits to the retired parent will remain and can be transferred to the second generation without triggering tax.

Sale of a business

Some small businesses are sold to family members or partners. The proceeds from these types of asset sales are treated as taxable income. By setting up an IPP and using terminal funding, a deduction can be created against this income.

Early retirement

Legislation requires funding projections to be based on a retirement age of 65. However, any time after reaching age 60, a member of an IPP can retire and supplement the benefits provided in the plan by adding unreduced early retirement benefits, cost of living increases, and bridging benefits. These early retirement benefits can provide a significant tax deduction for the company.

Ideal candidates

- Owners of an incorporated company

- Individuals age 40 or older

- People who earn employment income of at least $171,000, reported on a T4, from the company sponsoring the IPP

Take action

- Request a quote from your advisor showing the deposits that can be made based on your age and length of service while incorporated.

- Compare the benefits of an IPP to an RRSP.

- Work with your advisor to establish an IPP if you determine it’s right for you.

Contribution comparison 2022

Investment options available through Manulife Investment Management

Manulife and its subsidiaries provide a range of investments and services. Manulife is committed to providing quality investment products and services so you can enjoy life and worry less.

Mutual funds

Mutual funds can help meet your specific financial needs throughout your life. Whether you’re just starting out, accumulating wealth, or nearing/in retirement, mutual funds offered by Manulife Investment Management can provide you with solutions to help build a portfolio that meets your needs.

Segregated fund contracts

For conservative investors looking to grow their wealth but who are also concerned about minimizing risk potential, segregated fund contracts may be an ideal solution. The appeal of these contracts is the combination of the growth potential offered by investment funds and the unique wealth protection features of an insurance contract.

Segregated fund contracts have many estate planning benefits that can help transfer wealth to the next generation quickly, privately, and efficiently. They can also minimize investors’ exposure to risk through death, maturity, and, in some cases, income guarantees, and they also offer potential creditor protection features — all from a single investment. These contracts may be ideal for mature investors planning their estate, investors concerned about the effects of market volatility, and small business owners. However, with an IPP, the annual pension required to be paid at retirement will usually be greater than the income guarantees offered by a segregated fund contract with an income benefit guarantee. Therefore, this type of product may not be ideal as an investment held by an IPP trust.

Guaranteed interest contract

For individuals seeking a guaranteed rate of interest while protecting their initial investment, a guaranteed interest account (GIA) may be a suitable option. GIAs available from an insurance company may also offer unique protection features, such as the potential for protection from creditors, plus estate-planning benefits. For Canadians looking for a low-risk investment with a guaranteed rate of interest, Manulife Investment Management GIAs may offer benefits that are different than other financial institutions’ guaranteed investment certificates.

1 Includes a spouse or common-law partner, as defined by the Income Tax Act (Canada)

![]()