Protecting your nest egg after you’re gone—annuity settlement option

Investment insight

You’ve worked hard over the years to make sure your loved ones will be comfortable—both now and after you’re gone. However, your nest egg can disappear very quickly when it’s passed on to your beneficiaries. This “sudden wealth” approach to transferring hard-earned savings is a real concern for many people.

For those who prefer to transfer an inheritance gradually over time, the most common approach in the past has been to establish a trust—either inside or outside the will—to control the estate after death. Trusts can be a very effective wealth transfer vehicle, but there are some drawbacks that should be carefully weighed, such as cost, complexity, and ongoing management.

Annuity settlement option

There’s now another appealing wealth transfer option available to Canadians, which has considerable merit due to its simplicity and flexibility. The annuity settlement option from Manulife Investment Management can automatically transfer the proceeds of your insurance contract or policy into an annuity on death. The resulting annuity will then make gradual income payments to your beneficiaries, as specified by you.

It’s a simple, inexpensive, and effective wealth-transfer tool. It gives the advantage of replacing a lump-sum death benefit with smaller, scheduled payments while offering savings of legal, estate administration, and probate fees. In addition, it can provide increased privacy1 and potential creditor protection.

Unlike trusts, which can incur contract preparation costs and annual trustee and accounting fees, the annuity settlement option has no fees or ongoing management requirements. It’s a strategy that’ll appeal to most investors, regardless of whether the amount of the inheritance will be $50,000 or $1 million.

With the annuity settlement option, you have complete control over the specific annuity terms. You can select an annuity that makes payments to your beneficiaries for the rest of their lives or for a specific time period following your death.

Guarantee options can also be added to make sure a minimum amount is paid to your beneficiaries. This helps avoid a problem with wills that specify an annuity be purchased but are vague as to the type and terms, often leading to confusion or an undesired result.

If you decide to change the beneficiaries or terms of the annuity, all you and your advisor need to do is submit a new beneficiary designation online or complete the Beneficiary Designation—Annuity Settlement Option form (log-in required) at no cost instead of having to pay a lawyer to amend or redraft your trust agreement.

And if you have multiple beneficiaries, that’s not a problem. The annuity settlement option allows you to differentiate between beneficiaries, permitting some to receive a lump sum and others to receive an annuity based on the terms that you select.

What’s an annuity?

An annuity is an insurance contract where, in exchange for a single lump-sum deposit, an insurer makes guaranteed regular income payments to the owner of the annuity. These payments contain both interest and a return of principal component. Annuity payments can continue for a chosen period of time or for the lifetime of one or two people.

Which insurance contracts or policies qualify?

The annuity settlement option can be added to:

- Manulife Investment Management guaranteed interest accounts (GIAs)

- Manulife Investment Management segregated fund contracts

- Manulife Financial life insurance policies.

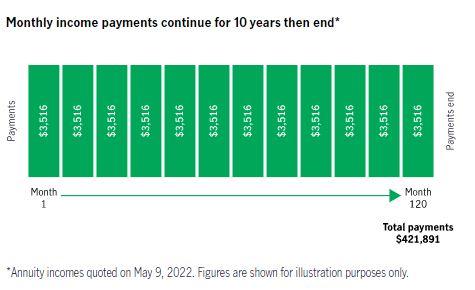

Richard and Joan—an example

Richard and Joan have $400,000 invested in a Manulife Investment Management segregated fund contract, which they want to leave to their son, Scott, in the event of their deaths. But Richard and Joan are concerned about Scott’s ability to manage this money and prefer to have the proceeds and future interest paid out to him over a period of time. After discussing the situation with their advisor, they select a 10-year term certain annuity settlement option on their segregated fund contract. Now, Richard and Joan have the comfort of knowing their estate will pass gradually to their son over a 10-year period after their deaths.

Estate benefits

The annuity settlement option offers many estate benefits:

- allows you to control the manner in which your assets are allocated to your beneficiaries

- eliminates the need and cost associated with setting up a formal trust

- provides an increased level of privacy while avoiding costly probate and estate fees

- makes sure that younger beneficiaries, such as children or grandchildren, receive a controlled income stream rather than a large lump-sum amount

- gives parents with disabled children a comprehensive estate-planning tool

- allows you to make changes to beneficiaries and settlement options quickly and without fees.

Minors and mentally infirm individuals

The annuity settlement option may also be effective for minor children or for beneficiaries with an impairment in mental functions. However, instead of naming these people directly as a beneficiary, a trustee (such as a family member) should be named “in trust for” these individuals.

The bottom line

If you don’t want to risk transferring your assets in one large lump sum after your death, you should take the necessary steps now to protect your estate. For those who prefer a highly structured approach, a formal trust should be investigated. If you prefer a simpler approach, the annuity settlement option from Manulife Investment Management may be just what you’re looking for.

1 In Saskatchewan, jointly held property and insurance policies with a named beneficiary are included on the application for probate despite the fact that these assets don’t flow through the estate and aren’t subject to probate fees.