The market developments

Dear friends,

I hope that you and your family are well. After a truly unique quarter for capital markets, I am writing to provide you with a brief overview of some key developments during that time, as well as some insight on what can be expected as we head into the next three months of the year.

While the first quarter of 2020 was dominated by anxiety surrounding the initial outbreak of COVID-19 and the ensuing lockdowns and capital market declines, the second quarter demonstrated a remarkable bounce back in those markets – even with a resurgence of the virus in the U.S. and renewed lockdown measures.

The S&P 500 Index, a broad measure of U.S. equities, had its best quarter in over 20 years, gaining 19.95% (in U.S. dollars), while the Canadian S&P/TSX Composite Index gained almost 16% (in Canadian dollars) in the three months ending June 30. This was quite a recovery from the sharp declines by the end of Q1, bringing year-to-date returns to -4.04% (S&P 500) and -9.07% (S&P/TSX). Government bonds declined as both the Federal Reserve (the Fed) and Bank of Canada indicated rates would remain low for a lengthy period.

Energy prices rose as the economy began slowly re-opening and production cuts trimmed inventory, but not before prices fell below zero for the first time in history on April 20, ending the day at -US$37.63. This served as a microcosm of the quarter. While virus data, economic numbers and other headlines seemed bearish, markets remained optimistic and continued to climb.

Much of the market’s enthusiasm has been attributed to government and central bank intervention designed to support global economies. In particular, the U.S. Federal Reserve’s introduction of quantitative easing measures, emergency lending and purchases of corporate bonds and exchange-traded funds are believed to have played a vital part in this rise. The Bank of Canada matched the Fed’s willingness to purchase corporate bonds to assist credit markets, while indicating it believes the economy will return to growth in the third quarter. The Fed said it expects 5% GDP growth in 2021, and as for the support it has been providing to the system, Fed Chairman Jay Powell said the agency was, “not out of ammunition by a long shot.”

Headlines concerning vaccine progress and phased economic re-openings also seemed to support market moves to the upside. Promising vaccine data from various companies continued to be announced, while in early May the U.S. Food and Drug Administration granted emergency use authorization for Gilead Sciences’ antiviral drug remdesivir as a treatment for COVID-19 patients.

Investors also weighed more negative developments as the quarter came to a close, but these had little impact on the markets’ recovery. These included escalating tensions between China and both the U.S. and India, rising infections in 37 U.S. states (with 50 per cent of states halting or rolling back their reopening plans), and data showing 31.5 million Americans collecting unemployment cheques as of mid-June. The Fed said it expects U.S. gross domestic product (GDP) to shrink by 6.5% in 2020, and the International Monetary Fund (IMF) expects global economic output to contract 4.9%. Ratings agency Fitch Ratings, meanwhile, downgraded Canada’s credit rating to AA+ from AAA to reflect the deterioration of public finances due to COVID-19.

If anything, the last two quarters have proven just how important it is to stick with a long-term, diversified plan to withstand market shocks. It would have been almost impossible to predict that shortly following the close of the first quarter, the S&P 500 would have the best 50-day period in its history and the Nasdaq (a stock exchange that includes the world’s primary technology and biotech giants) would reach new all-time highs. Had we chosen to change course and attempt to time the market, we may have missed out on this rapid recovery. I continue to believe that at times of great uncertainty, discipline and the ability to remove emotion from one’s financial decisions become an investor’s most valuable asset. These characteristics, combined with your trust in me to oversee your investment plan objectively, have allowed us to navigate that uncertainty in an effective manner.

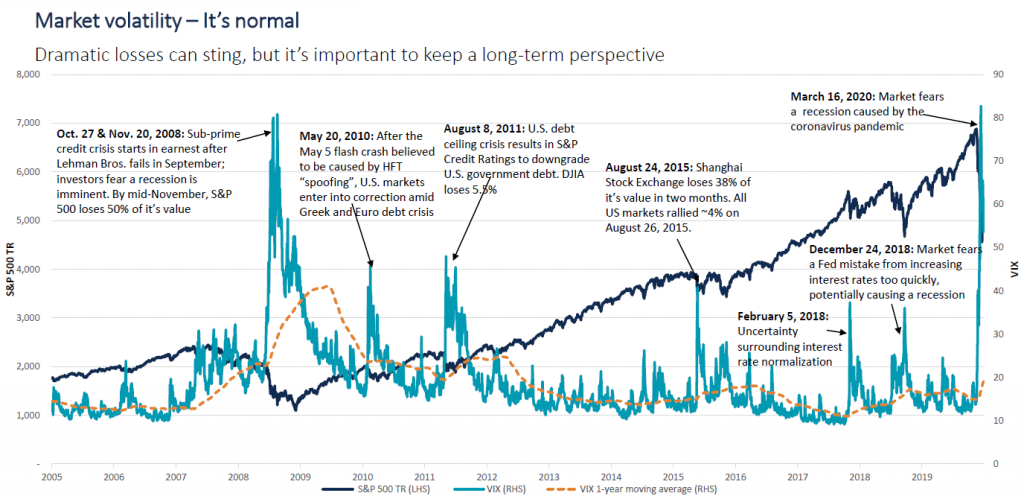

As we begin the third quarter, there is no way of predicting how the markets will react, and whether monetary and fiscal support will outweigh future outbreaks of COVID-19 and any subsequent economic disruptions. What we do know is that volatility remains a distinct possibility, and that history shows continuing to stick to a well-constructed, long-term plan has been the right move. The chart below illustrates this point nicely.

In closing, I wish you and your family well and remind you that I am always happy to discuss your investment plans. If you have any questions, please contact me at 450-951-8787

Sincerely,

Michel Prévost