Unknowns – Known and Unknown

The world is full of surprises or unknowns, some of which we can anticipate, while others are harder to foresee. “Known unknowns” are uncertainties and issues of which we are aware, but do not know the outcome. An example is this year’s U.S. presidential election. “Unknown unknowns” are events that we do not expect or have never happened before, such as the COVID-19 pandemic.

The COVID-19 pandemic has brought a new set of known unknowns. We know the virus exists, but do not know when and how the economy will recover, how many people will be infected, when a vaccine will be available, and how safe and effective the vaccine will be. The significant support to economies and capital markets from central bank interventions and government spending have eased some of these concerns. Just as we have not yet won the war against the virus, the long-term effects of its economic consequences remain to be seen.

Quantitative easing in the time of COVID-19

Quantitative easing (the increase of money supply in the economy from central banks) is not a new tool. It was first designed to combat the global financial crisis in 2009. From 2009 to 2015, the U.S. Federal Reserve injected $3.5 trillion into the economy, which led to asset inflation. To avoid a dramatic economic shock, the Fed retracted these measures very slowly. Over the course of approximately four years, the money supply shrank by about $0.8 trillion.

The Fed is using this same tool to fight the economic consequences of the pandemic, but with unprecedented speed. In just three months, $3 trillion was added to the economy. In that same time, cash went from being king (when markets were volatile) to trash (as supply increased). While quantitative easing has inflated asset prices, it has consequences – in other words, new known unknowns.

It is not certain how long this situation will last. It is estimated that the Fed’s balance sheet will be extended to $10 trillion and, if the past is any guide, will take three decades to return to pre-pandemic levels. If that is the case, asset prices will remain elevated as cash is devalued (30 years is effectively permanent). Asset holders will benefit the most, while savers suffer. This could amplify another growing issue – the wealth gap, a problem central banks have ignored in the past. Can they continue to ignore it for the next decade or even three?

Forever indebted?

In addition to quantitative easing, another by product of this pandemic was government spending in the form of subsidies to individuals and businesses. These totalled approximately 15% of gross domestic product (GDP) in both Canada and U.S. The challenge is not the subsidies themselves, but that both governments were running deficits prior to this and the extra burden adds uncertainty to how the debts will be repaid. Raising taxes is an obvious solution but could further weaken the economy and is politically unpopular. The only other solution is higher debt and larger deficits for longer – so long that many will see it as permanent. Large debt balances are only affordable if interest rates are zero, and who is going to save at zero interest?

The “new” new normal

The term a “new normal” was created after the financial crisis to describe a world where money supply is above trend and interest rates are below normal. After this pandemic, we will enter a “new new normal” where money supply is likely to be even more above trend and rates are close to zero for a decade, or decades. The unknowns in economies and human behaviour will continue to evolve in the next several years. Over the long term, there are very good odds stock markets will broadly outperform bonds, as yields are so low. Over the short term, there will be a tug-of-war between those who believe we will return to the “new normal” established in 2009 and those who believe we are headed to the “new new normal”. Either way, there is sure to be volatility, opportunities and challenges.

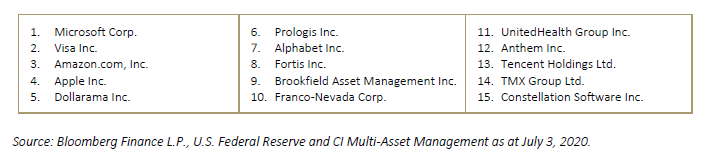

Combine top 15 equity holdings as of June 30, 2020 of the Evolution 40i60e Standard portfolio with Alpha-style exposure: