Ways to use a TFSA in retirement

During income-earning years, a Tax-Free Savings Account (TFSA) can be used to fund numerous expenses – a child’s education, family trips, a wedding, just about anything. Once you retire, you’ll discover that a TFSA is just as versatile, helping you to meet a variety of needs unique to retirement.

Continue to contribute

Many people in traditional retirement years still earn income from part-time work, consulting, a business or rental property. You cannot contribute new money to a Registered Retirement Income Fund (RRIF), but you can use your TFSA to continue making contributions to a tax-advantaged vehicle.

Even if you don’t have earned income, you may find that your minimum required RRIF withdrawal leaves you with more retirement income than you need. If you take a portion of the after-tax RRIF withdrawal and make a TFSA contribution, you allow the proceeds to grow tax-free.

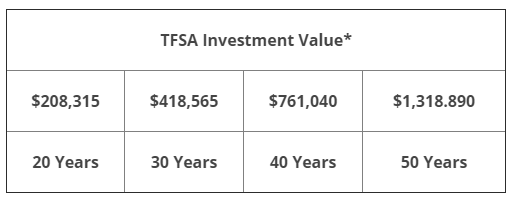

Another source can be investments in a non-registered account that you gradually transfer to a TFSA. Note that in making this move, non-registered investments are taxable when they’re sold or transferred in-kind, but they would always be subject to tax eventually. This way, you pay tax now, then benefit from future tax-free growth and tax-free withdrawals.

Draw tax-free income

The ability to draw income that’s completely tax-free makes a TFSA a flexible tool to carry out a number of retirement income strategies. Here are just a few examples of many applications.

Say that a retiree requires more income in a particular year, but sits at the upper threshold of a tax bracket. Instead of drawing taxable funds that would be subject to greater taxation, this individual could withdraw TFSA funds.

Similarly, a retiree could be in a position where additional retirement income, needed to support their lifestyle, would result in a clawback of Old Age Security (OAS) benefits. Withdrawing from their TFSA solves the problem as these non-taxable funds aren’t included as income for tax purposes.

A retiree could be following a strategy that defers Canada Pension Plan (CPP)/Quebec Pension Plan (QPP) and OAS benefits to age 70, aiming to maximize the benefits’ value over time. During the years before their government benefits begin, the retiree can access tax-free TFSA funds to supplement other sources of taxable income.

Tax-free funds are also practical to cover large expenses, such as renovations, travel or long-term care. In this case, there’s the option to replenish the TFSA with funds from a non-registered account.

Leave tax-free funds

TFSAs can be ideal in planning your estate, as you can leave funds to a beneficiary without the need to plan for taxation.

If you have a spouse, it’s usually best to designate each other as “successor holder.” This way, the successor holder simply takes over the late spouse’s TFSA without any complications. It’s hassle-free and a simpler transaction than naming a spouse as beneficiary. But if you’re leaving TFSA assets to a child or other heir, you do designate them as beneficiary, and they’ll receive the proceeds tax-free.

A TFSA can be used to help offset an estate’s tax liability. One way is to name the estate as beneficiary, so TFSA assets can be applied to the tax payable. Another way is to name a charity as beneficiary, in which case the charity receives the proceeds, and tax can be offset by the donation tax credit.

![]()