When should you start CPP/QPP and OAS benefits?

Start government benefits sooner and you collect a smaller monthly benefit, but right away and for a longer time. Delay the start and you receive a larger monthly benefit, but must bridge the waiting period with other resources.

Knowing when to start isn’t always easy, and even many financial experts offer vastly different opinions. Some retirement planners say to begin Canada Pension Plan (CPP)/Quebec Pension Plan (QPP) benefits as soon as you retire, even if it’s age 60. A recent report from the Canadian Institute of Actuaries recommends deferring the start of CPP/QPP benefits, even to age 70.1

To help understand the situation, here’s a look at key reasons why Canadians choose to start benefits sooner, later, or at the traditional time.

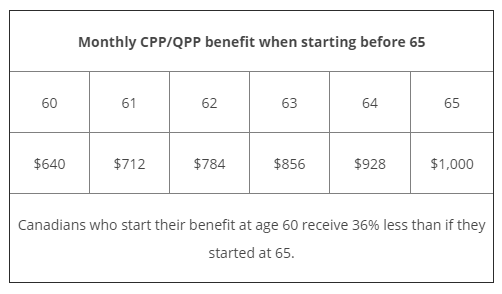

Starting before 65

One reason someone may start CPP/QPP benefits before age 65 is quite simply that they have retired and need the money to meet retirement income needs. Another is having a medical condition or illness that causes concern over a shorter-than-average life expectancy, prompting the individual to take advantage of benefits now.

Some people choose to collect CPP/QPP benefits sooner even if they have considerable sources of retirement income. Outlasting their savings is not an issue, so they start government benefits now, preserving more of the funds that may ultimately go to the next generation.

This chart uses $1,000 as the age 65 monthly amount. The maximum monthly benefit for 2021 is $1,203.75. The average amount for new beneficiaries was $689.17 (October, 2020).2

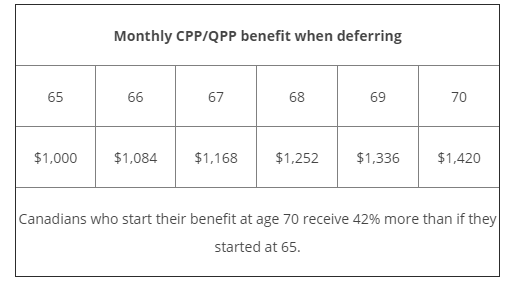

Deferring to after 65

A clear situation where someone may choose to defer benefits after 65 is if they’re still working full-time. First of all, they won’t need the extra money. Second, CPP/QPP benefits increase income and are taxable, so taking benefits could result in a larger tax bite.

Some retirees may choose deferral to receive a greater amount of total benefits over time, counting on living to the average life expectancy or longer. By their early 80s, a retiree who started CPP/QPP benefits at 70 would accumulate more total benefits than if they had started at 65.

Starting at 65

A retiree may start benefits at age 65 instead of deferring because they’re counting on the funds to support their retirement lifestyle.

But even if a retiree has the resources to easily make the deferral, they may still decide to begin CPP/QPP benefits at 65 because they feel uncomfortable turning down years of benefits. Take the example of the above chart. A person who opted for $1,000 per month of CPP/QPP benefits at age 65 would have received $60,000 by age 70. Say that they also began the Old Age Security (OAS) benefit at age 65 ($615.37 monthly as of March, 2021), instead of deferring OAS to age 70. That person, by age 70, would accumulate government benefits of almost $100,000.

Making your decision

As you can see, there are various reasons why it can make perfect sense to start government benefits at age 60, 70 or any age in between. Sometimes it’s about the math, and other times it’s personal.

We encourage you to speak with us when it’s time for you to choose. Often the timing decision involves coordinating government benefits with retirement income you withdraw from registered and non-registered sources. Tax implications can affect timing. Also, we can discuss various timing strategies with you. For example, if you have a spouse, you can potentially choose four different years to begin receiving CPP/QPP and OAS benefits.

Calculating the benefits

You can choose to receive CPP/QPP benefits as early as age 60 or as late as age 70. The monthly benefit is based on the amount you are entitled to receive at age 65. If you begin earlier, the age 65 benefit amount is reduced by 0.6% for each month before 65, a decrease of 7.2% per year. If you defer benefits, the age 65 amount is increased by 0.7% for each month after 65, an increase of 8.4% per year.

OAS benefits normally begin at age 65, but you can defer the payments up until age 70. By deferring, the amount you would have received at 65 is increased by 0.6% each month, a 7.2% increase per year. That’s a 36% increase when deferring to age 70.

For CPP/QPP and OAS, the monthly benefit amount you start with remains the same for as long as you live, except for increases tied to inflation.

![]()