Don’t be so negative: Three-minute macro

Earnings estimates have started to decline, but some sectors are doing far better than others. We also take a look at European trade dependence and how different commodities might perform in a slowing economy.

Negative earnings revisions are just the beginning

Forward earnings-per-share (EPS) consensus estimates for the S&P 500 Index likely peaked on July 6 for this cycle and have only retraced 1.3% since that point. In a previous three-minute macro, we explained that earnings typically peak on average just 42 days before the official start of a recession, and looking at the past four recessions, the maximum EPS drawdown from the peak was 28%. While EPS revisions have been trending downward for more than 4 months, history would suggest there’s still a ways to go.

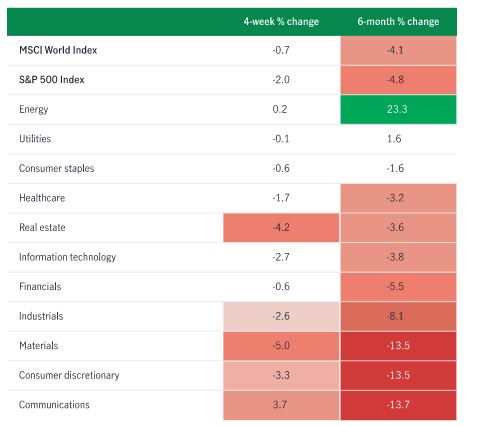

We think that inflation has been flattering earnings estimates, allowing them to appear artificially higher, but some sectors have been feeling the pain more than others: Communications, consumer discretionary, and materials have seen the sharpest downward revisions over the past six months, coinciding with current macro forces. Many of the underlying materials companies have seen downgrades in more cyclical segments of the commodity space such as base metals, whose outlook is challenged due to slowing growth. Similarly, Amazon, which is an outsize weight within the consumer discretionary sector, quoted several macro headwinds as key reasons their most recent earnings report missed consensus. Conversely, the biggest index weights—IT, healthcare, and financials—have seen modest declines, which explains why overall index-level expectations have stayed relatively high. Over the past month, a standout sector has been real estate, which had among the sharpest negative revisions, a result of the rerating higher of the terminal rate expectation, which will unequivocally put pressure on real estate investment trusts. We aren’t surprised to see energy being the only sector that’s seen positive revisions on both the one- and six-month basis given the acutely tight supply side.

Overall, the third quarter’s earnings season confirmed the softening that many of our leading indicators are suggesting, but with forward earnings only retracing about 1% from the peak, we believe that most equity classes will remain under pressure as earnings expectations continue to erode.

The earnings decline is on

Forward EPS revisions

Source: Bloomberg, Manulife Investment Management, as of November 14, 2022. EPS refers to earnings per share.

European trade dependence

German trade dependence can’t be understated. Chancellor Olaf Scholz’s recent trip to Beijing highlighted Germany’s trade relations with China at a time when political dynamics are tense, and it’s clear that shorter-term business and economic interests were prioritized.

Messaging from Europe’s largest economy and exporter is in contrast with our strategic view of U.S. hegemony, but a look at German trade balances with China over the past two decades explains why: Germany leads European exports in autos, industrial equipment, and pharmaceutical and chemical products. Outside of the Netherlands, China is Germany’s largest trading partner (surpassing even the U.S.), and trade between the two nations has been rising. In U.S. dollar terms, Germany’s imports from China have recently exceeded their exports, creating a negative trade balance for the first time in a decade.

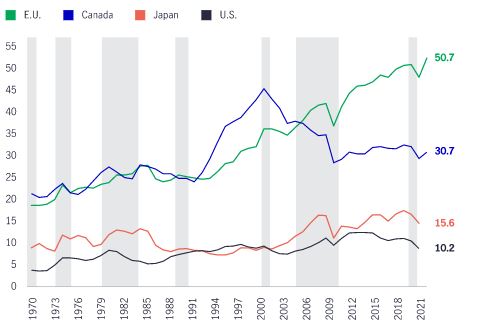

This new reality means European trade dynamics are at risk. With U.S.-Chinese economies decoupling amid heightened geopolitical tensions, risks are rising for European economies, which are so heavily dependent on Chinese trade and business. In the event that an export-driven economy shifted its trade dynamics, a stagflationary shock is likely to persist. Exports as a percentage of GDP for the European Union have been rising—something that hasn’t been the case for many other developed-market economies, including Canada, the United States, and Japan. Shifting trade dynamics would put downward pressure on exports and, therefore, growth (namely industrial production and employment) and upward pressure on inflation, as sourcing goods would be increasingly costly. From a longer-term perspective, terms of trade would likely put downward pressure on the euro.

Exports are increasingly important for European GDP

Exports of goods and services (% of GDP)

Source: World Bank, Macrobond, Manulife Investment Management, as of November 14, 2022. Gray bars indicate U.S. recessions.

Not all commodities are created equal

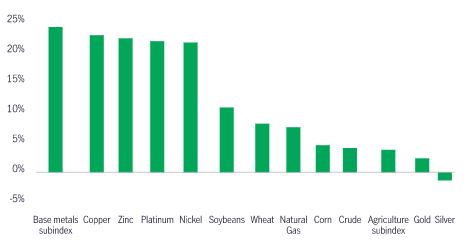

We’ve been bullish on the energy and agriculture subindexes of the commodity space throughout the pandemic, and our recent research suggests that this strength could persist even through a deteriorating macro backdrop. We ran a regression with global Purchasing Managers’ Indexes and various commodities, and the results are clear: Base metals have held a closer relationship to economic activity than energy, agriculture, or precious metals. This makes sense as demand for base metals is more cyclical in nature, which explains why they’ve struggled this year. In contrast, the demand for many agriculture products is relatively inelastic, and studies that look at oil demand through recessions prove that crude demand tends to be modestly resilient during recessions.

The supply side of both agriculture and energy is tightly constrained, and this isn’t something that central banks have the ability to directly control. Arable land relative to protein consumption has been tumbling for years, and climate change and extreme weather events will continue to wreak havoc on crops. It’s also been evident that years of underinvestment in both traditional and less carbon-intensive energy capital expenditure have led to a tight supply side for all energy sources. While agriculture and energy commodities are some of the only positive-returning assets this year, a less-cyclical demand profile and acutely tight supply side support our view that these assets can still outperform over the medium term.

Not all commodities are created equal

Selected commodities’ correlation to global PMIs

Source: Macrobond, Bloomberg, Manulife Investment Management, as of November 14, 2022. PMIs refers to Purchasing Managers’ Index.

![]()