Dull, boring, repetitive … the investment case for high-quality dividend growers

“If investing is entertaining, if you’re having fun, you’re probably not making any money. Good investing is boring.”

– George Soros

Regardless of the causes of recessions and their nuances, high-quality dividend payers and growers perform well prior to, during, and after a recession. Where it’s impossible to “time the recession,” an asset allocation that consists of a sleeve of high-quality dividend growers is important for risk-adjusted returns.

There has been an increase in chatter of a recession after the surprising announcement that the U.S. economy contracted by 1.4%, on a seasonally adjusted and annualized basis, for the first quarter of 2022. While we were surprised at the negative announcement, we maintain our stance that a typical recession in 2022 remains a low-probability event.

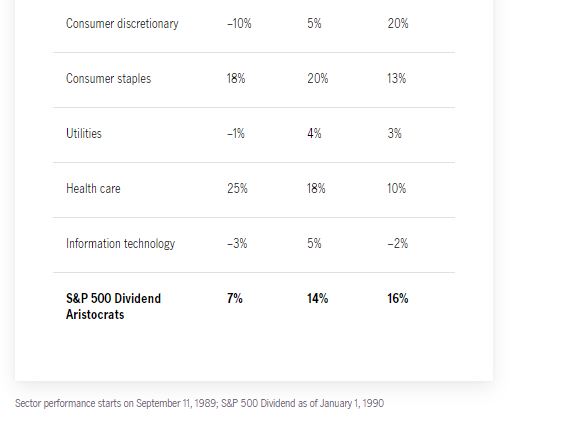

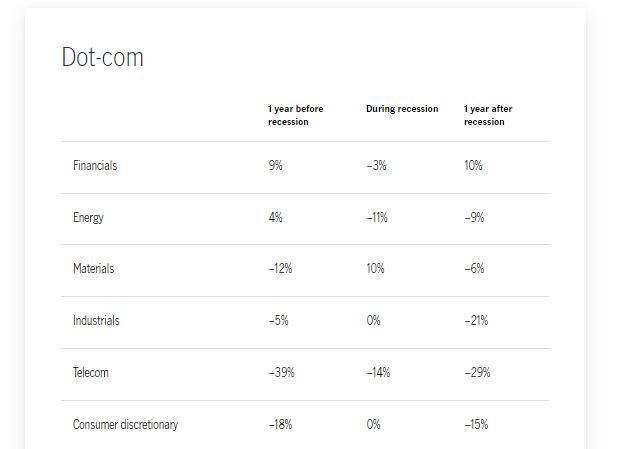

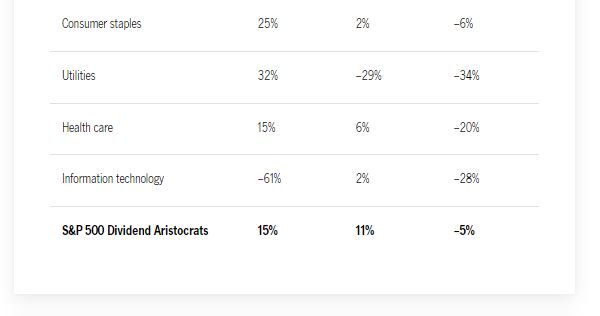

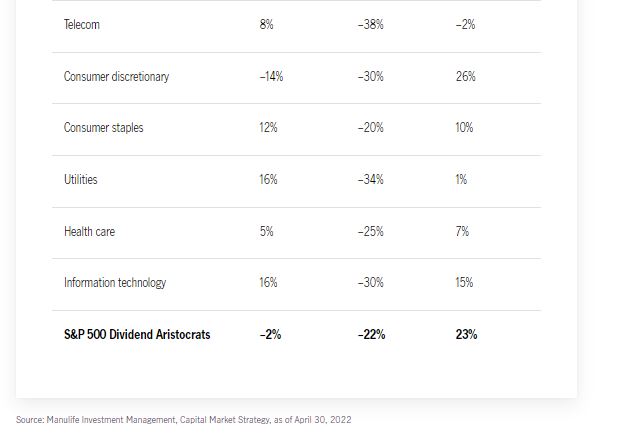

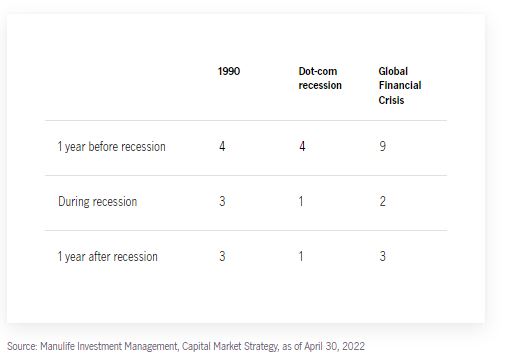

With the increased chatter of a recession (not our base case), we’ve received requests for sector performance during previous recessions. The data doesn’t go further than 1990 for the S&P 500 GICS (Global Industry Classification Standard) sectors, as the data originated on September 11, 1989—as per the S&P Global website. As a result of the limitation in the data, we looked at the previous three recessions: 1990–91, dot.com, and the Global Financial Crisis—we didn’t look at the “COVID recession” since it was self-induced. We looked at sector performance one year before the recession, during the recession, and one year after the recession. It should be noted that when comparing environments, there are nuances—we’ve defined these nuances in the “Appendix of this article.

Not surprisingly, as the tables illustrate, there’s no consistency among sectors through the different recession periods. As indicated above, each period has individual nuances. We included the S&P 500 Dividend Aristocrats Index (an index that consists of companies that have grown their dividend in each of the last 25 years) as a proxy for quality businesses and the findings were very interesting. In the table below, we show where the S&P 500 Dividend Aristocrats Index ranks among the ten sectors in each period during the various recessions. The lower the number, the higher the ranking. For example, the S&P 500 Dividend Aristocrat Index ranked 1 of 11 during the dot-com recession. Regardless of the recession and each one’s individual characteristics, high-quality dividend payers and growers performed well prior to, during, and after the recession.

What are high-quality dividends?

- Dividends that are supported by companies whose earnings remain resilient through different economic cycles (high percentage of recurring revenue)

- Dividends that are supported by a business that can invest in organic growth while expanding margins

- Dividends that are supported by a business that have pricing power and opportunities to grow market share

- Dividends paid by companies that have high and consistent return on equity

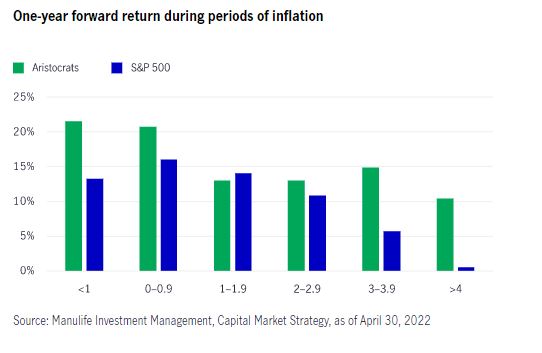

Over the next couple of months, we believe inflation will likely peak and trend lower from the current level of 8.5% as measured by the Consumer Price Index. It’s unlikely to fall to levels that were present prior to the pandemic as a result of higher wages, as well as energy and food costs. Inflation will remain a concern throughout 2022 but will likely receive nowhere near the level of attention it’s receiving today.

As the chart below illustrates, high-quality dividend growers outperform their broad, large-capitalization U.S. peers in most inflationary environments. With inflation likely to remain higher than 3% throughout the next year, high-quality dividend growers are positioned to do well.

There has been no shortage of risks in 2022

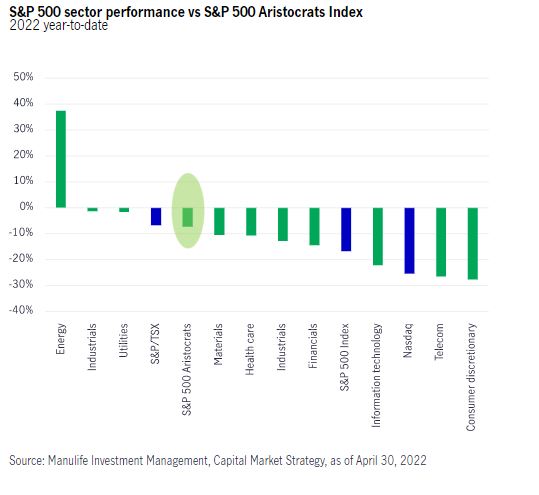

This isn’t the most severe global economic backdrop but it’s one of the most complicated. The complicated backdrop includes levels of global inflation not seen in decades, supply chain disruptions, conflict in Europe, and COVID-19-related shutdowns in China. Despite the uncertainties, we’ve witnessed the benefits of quality dividend growers in year-to-date performance. The S&P 500 Aristocrats Index has underperformed only in the energy, utilities, and industrial sectors. Moving forward, high-quality dividend growers are likely to have less volatility than the energy sector and more growth than the utility and infrastructure sectors, which are typically very defensive sectors with little room for growth.

Regardless of the recession and their nuances, high-quality dividend payers and growers perform well prior to, during, and after the recession. Where it’s impossible to “time the recession,” an asset allocation that consists of a sleeve of high-quality dividend growers is important for risk-adjusted returns.

Appendix

It should be noted that when comparing environments, there are nuances, including:

- Distribution of sector returns is so wide that the average doesn’t necessarily instill confidence.

- Types of companies within sectors have changed over time (e.g., information technology).

- Sectors are very heterogeneous. Companies within sectors are so different (e.g., Best Buy and Hillenbrand).

- Each period has individual nuances. What were the inflation numbers, interest rates, causes of recession, etc.?

- There are new sectors today that didn’t exist before. (e.g., real estate, communications)

- There’s a survivorship bias (some companies no longer exist).

Sector performance one year before, during, and one year after the 1990 recession, dot-com recession, and Global Financial Crisis recession