Rising rates and real estate: Three-minute macro

A hawkish BoC should have Canadian homeowners on watch as interest-rate rises will likely eat into their purchasing power. We also break down why green energy stocks are underperforming this year and why stagflation is such a scary word.

Hawkish BoC may mean pain for Canadian homeowners (and consumers)

The Bank of Canada (BoC) is one of the most hawkish developed-market central banks, and while there are clear headwinds to the real estate sector in the country, we think the stress that the BoC will add to the Canadian consumer through likely rate hikes is underappreciated.

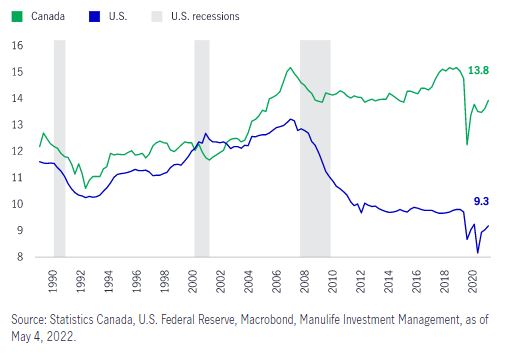

Critically, approximately 30% of Canadians have some form of a variable rate mortgage, much greater than in the United States. Additionally, Canadians carry higher debt loads than their neighbors to the south, with debt-to-service ratios of about 13.8% to Americans’ 9.3%. With markets pricing 50 basis point hikes at the BoC’s June and July meetings (and continued hikes later in the year) paired with the interest-rate sensitivity of the debt loads, we see pain for the Canadian consumer ahead. A sizable increase in mortgage costs will erode real household disposable income and ultimately weigh on consumption demand—more money spent to service their mortgages means less available to pay for goods and services. We’ve always cautioned against underestimating the U.S. consumer, but their Canadian counterparts don’t have the same resiliency, and given their debt loads, the outlook for the Canadian consumer looks challenging as the BoC engages in a very aggressive tightening cycle.

Adding fuel to the fire, with Canadian residential investment (as a share of GDP) three standard deviations above the 60-year average, it’s clear the growth levels seen in Canadian real estate are unsustainable, meaning the market is likely due for recalibration and deceleration. A decline is housing sales activity will immediately create a drag on the transfer costs component of GDP, which has been elevated due to high sales volumes.

Rising rates are a headwind for Canadian consumers

Household debt service ratio, Canada vs. the U.S.

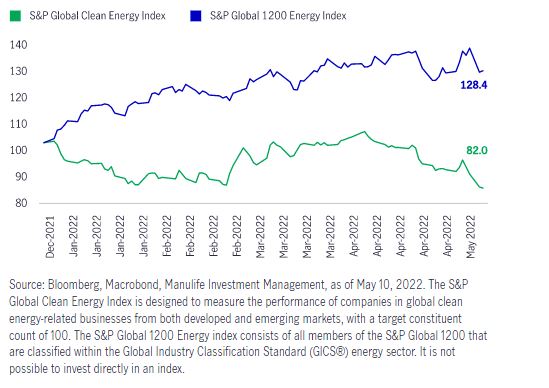

Clean energy is underperforming so far this year

As of this writing, the S&P Global Clean Energy Index has declined 18%, while the S&P Global 1200 Energy Index has increased by 28%. The Russia-Ukraine conflict has exposed the vulnerabilities in global energy sources, pushing up the price of crude oil, natural gas, and coal. As such, dirty energy companies—those that use fossil fuels and other sources of energy that aren’t climate friendly—have materially outperformed despite being on the wrong side of the environmental movement among investors. But that’s not the whole story, as there are other factors contributing to a weakening green energy sentiment:

- Long duration equities have underperformed both the broader regional indexes and short duration equities year to date. Given that many green names are inherently long duration in nature (e.g., clean tech stocks), the material move upward in yields over the past few months presents headwinds to valuations.

- Valuations for clean energy names are rich. At the end of 2021, the forward price-to-earnings ratio for the S&P 500 Index was 22.7x, compared with 36.8x for the S&P Global Clean Energy Index; as of this writing, they’ve backed down to 20.2x and 32.0x, respectively. While both indexes have experienced multiple contractions, it’s been particularly meaningful for traditional energy sources as their earnings have strengthened.

- U.S. policy can no longer be relied on to be a tailwind at the back of clean energy names. Democrats have struggled to pass new fiscal stimulus packages, and expectations for a Build Back Better package are deteriorating. This matters because the package initially included over US$500 billion in green spending, the largest environmental commitment from the country yet. With high odds of the Republicans taking control of the House in midterm elections this fall, these progressive climate initiatives face further headwind.

Clean energy has underperformed traditional energy year to date

Performance of global green energy vs. traditonal energy,

rebased to December 31, 2021 = 100

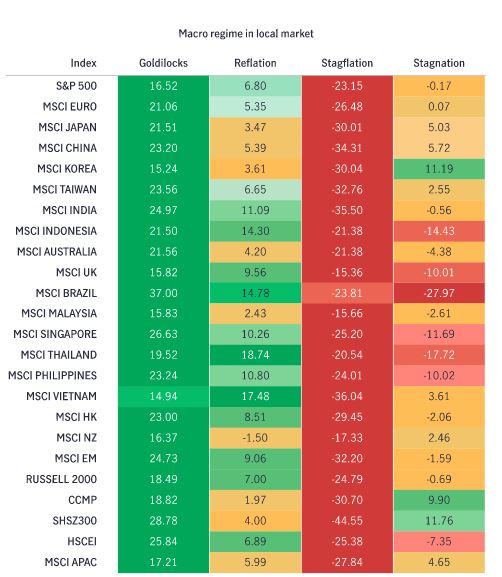

Why stagflation is a scary word

While inflation is all the rage these days, economic growth developments are equally important to the overall macro picture. Our framework summarizes the global macro backdrop under four potential regimes:

1 Goldilocks—Growth accelerating, inflation decelerating

2 Reflation—Growth and inflation accelerating

3 Stagnation—Growth and inflation decelerating

4 Stagflation—Growth decelerating, inflation accelerating

Stagflation is a scary word to investors, and asset class performance in different macro regimes shows why. We analyzed asset class performance under each of our framework’s regimes in various countries and regions. Perhaps unsurprisingly, the results show that stagflation has historically been the worst possible macro regime for risky assets, while outperformers have been the traditional safe havens—U.S. Treasuries, U.S. long bonds, Chinese and Japanese government bonds, and the U.S. dollar, Chinese renminbi, and Japanese yen.

The good news is that there are always investment opportunities, even in challenging macro conditions. We think that economies most insulated from the negative growth shock are those that are net food and energy exporters, are less reliant on foreign capital, and that still have policy space. At the same time, economies most capable of mitigating the negative supply shock are those that have a relatively lower weight for food and energy in their Consumer Price Index and import baskets. Balancing these considerations, our analysis suggests that within the Asia-Pacific economies we follow, relative macro outperformers are likely to be Australia, Indonesia, Malaysia, New Zealand, and Vietnam.

Why stagflation is a scary word

Regional returns (deviation from the mean) under different macro regimes

Source: Bloomberg, Manulife Investment Management, as of December 31, 2021. It is not possible to invest directly in an index.