U.S. dollar outlook—moving from strength to weakness

In early February, we noted that the U.S. dollar could be poised for a short-lived countertrend recovery, driven by U.S. political developments and their implications on fiscal policy and growth. We now believe that moment has passed and that the greenback is ready to enter a period of weakness.

The U.S. dollar (USD), as referenced by the U.S. Dollar Index (DXY¹), climbed nearly 5% between early January and March 31.² We now believe that the DXY is poised to resume its long-term downward trend, particularly with reference to the euro.

The USD is priced for perfection

To a large extent, the speed at which the U.S. fiscal picture evolved after the Georgia Senate runoff caught market participants off guard and accounted for much of the USD’s strength in Q1. However, we believe the USD is unlikely to appreciate further in the near term because the market has already priced in expected U.S. economic outperformance, driven by the great reopening and the acceleration in the country’s vaccination program.

From here, we expect growth and interest-rate differentials between the United States and developed-market economies to narrow as market participants look beyond the near-term U.S. fiscal outlook and incorporate their expectations for the medium-term cyclical picture.

Challenges to the U.S. growth outlook include a fading of the fiscal impulse—driven in part by the anticipated changes to tax policies—and the possibility of a short growth cycle. In other words, we believe the USD is priced to perfection. Indeed, the bar to upside surprises in the United States is exceedingly high, whereas expectations for Europe, Canada, and others have far more scope for positive shocks as we get closer to the second half of the year.

DXY correlations and valuation

Investors have historically relied on interest-rate differentials, also known as bond spreads, to assess the fair value of the exchange rate between two currencies, focusing on spreads at the shorter end of the yield curve (e.g., 2-year) to capture the outlook for relative central bank policy.

That said, market participants have begun to pay more attention to interest-rate differentials at the slightly longer end of the yield curve (10-year) in their analysis because they better capture the evolution in monetary policy in recent years where central bank asset purchases have become increasingly (perhaps permanently) prominent.

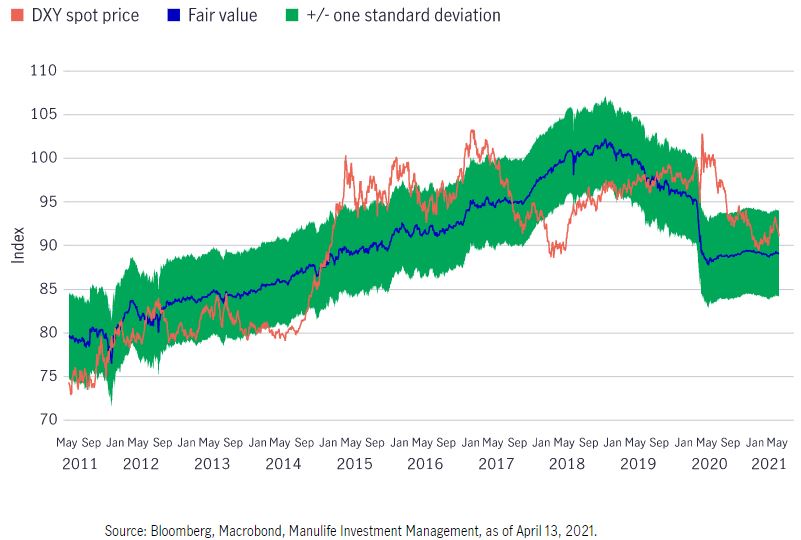

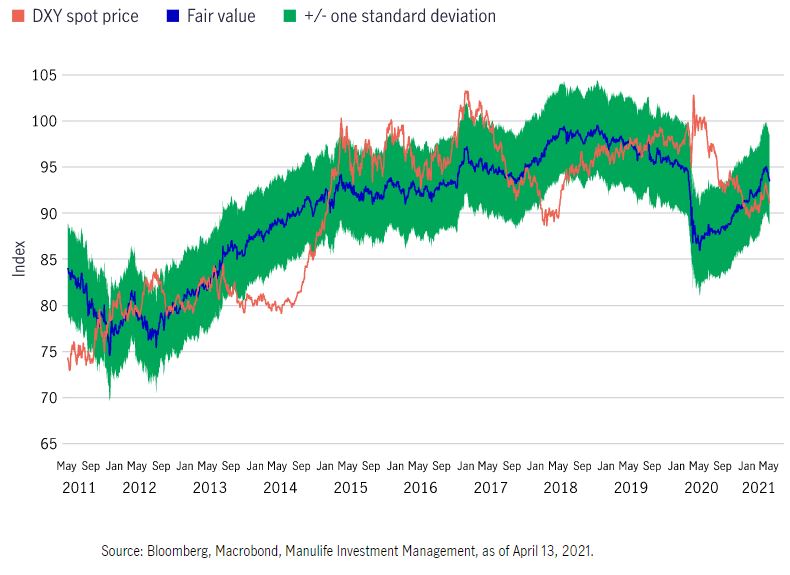

DXY fair value using weighted 2-year spread

And this is where it gets interesting: Using the DXY as a proxy for the USD, we compared the spot price for the DXY with the estimated fair value for the DXY based on the 2-year spread (interest-rate differential)—by this measure, the USD is overvalued. However, a similar calculation based on the 10-year spread suggests the USD is undervalued (although it’s closer to the estimated fair value relative to the first method).³

Of these, which is the better measure to use? Our analysis shows that the DXY’s correlations with the 2-year and 10-year spread are roughly equivalent on a longer-term basis. We also noticed that shorter-term dynamics are much more variable as the DXY’s correlations to bond spreads varied in intensity while also alternating between fundamentals (proxied through spreads) and market sentiment.

DXY fair value using weighted 10-year spread

Interestingly, at this moment in time, correlation studies revealed a relatively stronger relationship between the DXY and longer-term spreads; conversely, the correlation between the DXY and short-term spreads barely registered.³

Here’s our interpretation: USD strength that we saw in Q1 had been driven by changes in the U.S. 10-year yield, as markets began to price in monetary policy normalization (i.e., tapering as the U.S. Federal Reserve (Fed) scales back its various emergency programs)—but that’s now changed.

In our view, the Fed’s narrative will be a critical catalyst for the renewed weakening in the USD as market participants’ focus migrates from the back end of the yield curve and the tapering discussion toward the outlook for conventional policy and interest rates. The sequencing of Fed policy normalization—and its reflection in market pricing—is critical and explains some of the discrepancies we’ve observed in terms of the USD’s relationship to its fair value estimates.

Sentiment, positioning, and seasonal factors

Outside of fundamentals and sentiment, derivatives/options positioning and seasonal factors are also key considerations in regard to how the USD might perform in the coming weeks, and they appear set to complement (or at least not hinder) our expectations for a resumption of a weaker USD.

On sentiment, we note the recent developments in the options market: Risk reversals, which refer to the difference between the implied volatility between call options and put options, are threatening to head back into negative territory, thereby signaling that more investors are expecting the USD to depreciate than those expecting it to rise in value.

Weekly speculative futures positioning data from the Commodities Futures Trading Commission also reveals a significant liquidation of bearish bets against the USD in Q1. Current positioning also suggests that investors remain somewhat bearish about the USD.²

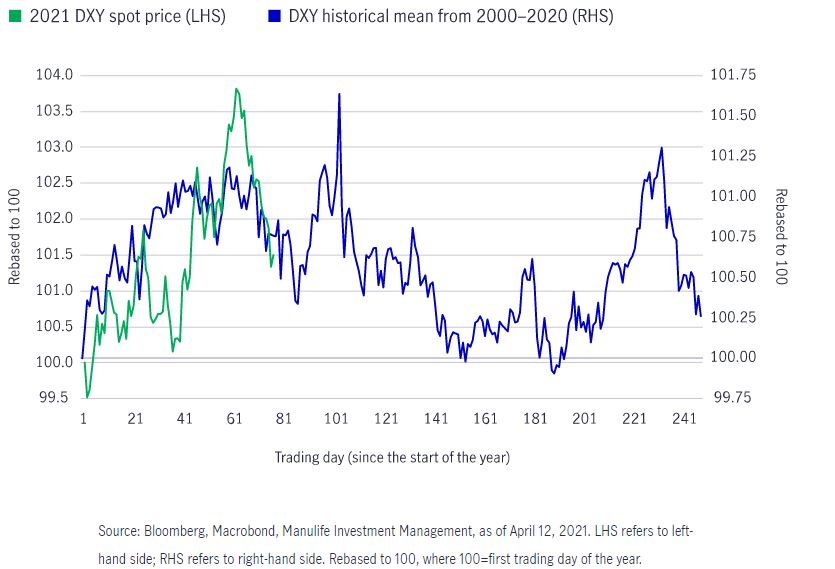

DXY seasonal trading patterns

Of the nonfundamental considerations, seasonal factors appear to offer the most compelling argument for a resumption of broad-based USD weakness. The USD tends to follow well-defined seasonal trends with a historically strong start to the year followed by weakness through Q2 and Q3 and renewed strength around the start of Q4. The DXY has delivered a near-textbook performance so far in 2021, suggesting that we could see weakness in the USD in the next couple of quarters.

Risks to our views

The primary risk to our bearish USD outlook relates to sentiment. The USD’’s role as a safe-haven currency means that our views will be vulnerable to a surge in geopolitical tensions since such events are likely to encourage investors to seek shelter in the currency. Similarly, any development that points to a meaningful disappointment in global economic fundamentals could also spark flows into safe-haven assets, including the greenback.

1 The U.S. Dollar Index is a measure of the value of the U.S. dollar relative to the value of a basket of currencies of the majority of the United States’ most significant trading partners. It is not possible to invest directly in an index. 2 Bloomberg, Macrobond, as of April 13, 2021. 3 Bloomberg, Macrobond, Manulife Investment Management, as of April 13, 2021.

![]()